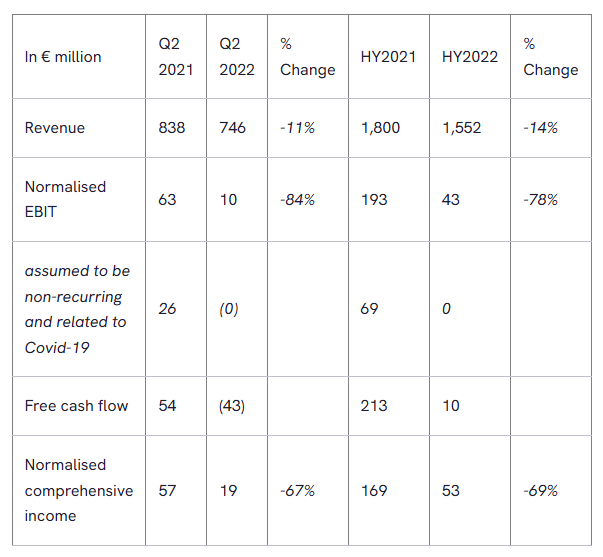

- High inflation and pressure on consumer spending impacted costs and development e-commerce volume

- Domestic volume growth at Parcels ~3%, excluding non-recurring impact related to Covid-19; overall, volumes -12.6% reflecting no further Covid-19 impact and development in cross-border activities

- Volumes at Mail in the Netherlands -7.4%, slightly better than expected

- Free cash flow performance reflects step-down in normalised EBIT and working capital phasing

- 20% improvement in carbon efficiency

- Interim dividend 2022 set at €0.14 per share

- Outlook FY 2022:

- normalised EBIT revised to €145 million - €175 million

- free cash flow of €110 million - €140 million, at lower end of initial range

Herna Verhagen, CEO of PostNL, said: “The current macroeconomic and geopolitical environment is challenging and causes headwinds, especially for the logistics industry. This is causing prolonged uncertainty and limits visibility on the development of consumer behaviour.

“An unprecedented high level of inflation resulted in rising fuel and labour costs and impacted our performance. We stepped up our actions on tight cost control and are taking adaptive measures to mitigate the ongoing headwinds. Clearly, these higher costs cannot only be absorbed through improved efficiency and productivity gains, but will also need to result in price adjustments going forward. At the same time we are maintaining our efforts to align our operations with anticipated volumes, while holding on to the necessary flexibility and desired quality level for peak season within the limits of the current tight labour market.

“Furthermore, inflation puts pressure on consumer spending, which has meanwhile rebalanced towards services since society reopened. This impacts parcel volumes and reduces predictability. Our market share remained stable. In this difficult environment, Mail in the Netherlands continues to deliver its solid performance.

“Taking into account the uncertain economic outlook and limited visibility, we are revising our FY 2022 outlook for normalised EBIT. Adjusting capex to align with volume projections and applying strict working capital management should allow for a delivery of a strong free cash flow at the lower end of our initial outlook range.